Pharma PLI needs to be revisited

The domestic value addition and bank guarantee norms are burdensome for a segment that is SME-driven

The recent data on India’s import of Active Pharmaceutical Ingredients (APIs) gives the impression that import dependence appears to be an unsolved puzzle. The Covid-19 pandemic exposed the vulnerabilities of global API supply chains focused on a single country, China, and a number of leading countries including India took initiatives to reduce their reliance on China.

An analysis based on UN Comtrade database, using a classification of pharmaceutical products based on International Standard Industrial Classification, shows that the reliance of countries on China has in fact increased during the post-pandemic period. China’s share in global import of APIs has increased from 18 per cent in 2019 to 24 per cent in 2022. China’s share in India’s import of APIs has also increased, from 70 per cent to 72 per cent during the same period. Despite the assertions of supply source diversification, countries’ reliance on China has increased.

Impact of the scheme

In this context, it is important to examine the impact of the PLI scheme aimed at incentivising indigenous production of those APIs [and key starting materials (KSMs) and drug intermediates (DIs)] in which India was heavily import dependent (PLI 1.0). There are 41 products covered by this scheme. Production under this scheme began 2022-23.

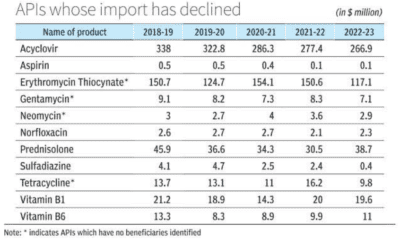

We were able to get product-wise import data for 18 out of the 41 products, at HS 8-digit level, for 2022-23 from the import data provided on the Ministry of Commerce and Industry website. It is found that in 10 products, the import value has declined in 2022-23 as compared to 2018-19, pre-pandemic period. And in the remaining eight products, the imports have increased.

One may tend to attribute the decline in the import of APIs to PLI 1.0. However, four out of the 10 products have no beneficiary identified yet. This indicates that firms’ own efforts, outside of the PLI scheme, to get out of over dependence on China is also very much in play. Unreasonable price hikes is a major reason that compelled some Indian firms to start producing indigenously. Therefore, it is not just the PLI incentives, but other forces are also at work in reducing import dependence.

The more pertinent concern here is the rising import value of some of the products covered by PLI 1.0. It may be possible that 2022-23 is the first year of production under this scheme and a better picture of the impact of the scheme may emerge in the following years. However, some observations on the design and implementation of the scheme indicate that there is scope for improvement to enhance the effectiveness of the scheme.

PLI 1.0 has 48 beneficiaries selected through four rounds of applications. A comparison of the final list of beneficiaries after each round shows that 17 beneficiaries exited from the scheme after they were selected. PLI 1.0 has a much higher withdrawal rate as compared to the second PLI scheme in the pharma sector (PLI 2.0) in which only two out of 55 beneficiaries exited, and were replaced. PLI 2.0 aims at product diversification to high-value goods and penetrating global value chains by the creation of national champions. The higher withdrawal rate in PLI 1.0 points to the need for improvement in the scheme.

Business model

APIs is a segment dominated by small and medium enterprises (SMEs). This is because the requirement of most KSMs and DIs is in small quantities and larger firms would not invest in producing so many KSMs and DIs.

Therefore, instead of producing in-house all the KSMs, DIs and APIs which are required in small quantities, large firms would tend to tie up with smaller firms for their supply. The business model of SMEs in this area is that they focus on one or a very few KSMs/DIs/APIs and they often do not get into the business of formulations. Given the dynamics of the industry, import dependence on KSMs/DIs/APIs cannot be addressed without giving due consideration to the SMEs. There are two major issues in the way the scheme is designed currently.

One, some firms find it difficult to meet the stipulated domestic value addition (DVA) requirements. DVA for fermentation-based products is 90 per cent and for chemical synthesis-based products is 70 per cent. Especially in those products where all the key inputs have been imported, replacing them with indigenous production all of a sudden to meet the value addition requirements is tough for smaller firms. Some firms have exited due to difficulties in meeting the DVA requirement. Development of KSMs in-house in a cost-effective manner requires technology efforts which takes time.

Second, the bank guarantee requirements for the beneficiaries of PLI 1.0 are exorbitant. Beneficiaries, mostly SMEs, are required to provide bank guarantees ranging from ₹20 lakh to ₹4 crore depending on the target group they belong to. Whereas in PLI 2.0, even the large firms having global manufacturing revenue of more than ₹5,000 crore need to furnish bank guarantees of only ₹1 crore and this requirement on MSMEs is only ₹5 lakh. It appears that the apprehension on meeting the DVA requirements and forfeiture of bank guarantee, in case of not meeting the committed production, prompted some beneficiaries to exit from the scheme.

Solving India’s API import dependence puzzle calls for modifications in the scheme, recognising the challenges and difficulties faced by SMEs, which are the dominant players in this segment.

The writer is a faculty member at the Institute for Studies in Industrial Development, New Delhi

https://www.thehindubusinessline.com/opinion/pharma-pli-needs-to-be-revisited/article68121968.ece